By Dan Mikes

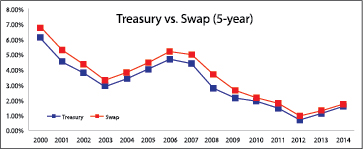

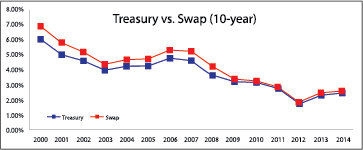

If you haven’t already heard while listening to the evening news, the 15-year historic graphs — shown, below — indicate that while interest rates are still relatively low, they might have bottomed and be on their way up.

While many think rates are likely to increase in the future, no one knows how much they will rise or when. Now might prove to be a good time to refinance existing debt and secure a long-term fixed rate if possible.

What if your religious institution currently has debt and the loan is subject to a prepayment penalty? If your leadership team believes rates are headed upward, it might make sense to pay the penalty and secure a lower rate now. But, how might you do the math to provide perspective on whether it would make sense to pay the penalty now? How much would rates need to increase to justify paying the penalty?

What if your religious institution currently has debt and the loan is subject to a prepayment penalty? If your leadership team believes rates are headed upward, it might make sense to pay the penalty and secure a lower rate now. But, how might you do the math to provide perspective on whether it would make sense to pay the penalty now? How much would rates need to increase to justify paying the penalty?

Running the numbers

The following hypothetical example is for illustrative purposes only. It might help your leadership team to answer these questions by providing some high-level perspectiv e. The template will enable your leadership team to identify how much rates would have to rise to justify paying the penalty and refinancing now. If your team feels rates will likely pass through the break-even threshold, you should refinance now.

e. The template will enable your leadership team to identify how much rates would have to rise to justify paying the penalty and refinancing now. If your team feels rates will likely pass through the break-even threshold, you should refinance now.

Let’s assume, for example, that four years ago your religious institution borrowed $5 million and the interest rate was originally fixed for five years at 6 percent, on a 25-year amortization. Your monthly payment is currently $32,215. Your lender tells you that if you refinance today, you face a prepayment penalty of $75,000.

You decide to shop around, and you receive an offer at 5 percent fixed for five years. Based on your current loan balance of $4,628,922, and your remaining amortization duration of 21 years, your new monthly payment would be $29,705.

While it’s great to see an immediate monthly savings and avoid the uncertainty of where rates might be as of loan maturity, we still haven’t identified how much interest rates would need to rise between now and your current loan maturity (12 months from now) to justify having paid the $75,000 penalty.

One way to answer this question is to compare the two scenarios — refinance now versus wait — in terms of total-out-of-pocket-expense over the next 60 months.

If you refinance now, your total payments over the next 60 months will equal $1,782,300. Add the $75,000 cost to exit your current loan, and your total out-of-pocket-expense increases to $1,857,300.

Conversely, if you stay with your current loan through maturity, your next 12 payments will total $386,580. When you renew your loan, if your new interest rate is 5.35 percent, your new monthly payment will be $30,723. Over the next 48 months, your total payments will be $1,474,704. Consequently, over the next 60 months the total out-of-pocket-expense equals $1,861,284.

Conclusion: Over the next 12 months, if your leadership team believes interest rates will increase 0.35 percent or more, fewer dollars will exit your pocket if you pay the prepayment penalty and refinance now.

Please note that the above example only considers out-of-pocket-expense. No cost has been assigned for the loss of investment income which might have been earned on $75,000 had it been retained rather than spent to satisfy the prepayment penalty. We also did not consider the financing cost should you desire to borrow the $75,000.

While no one has a crystal ball, presenting this type of analysis to your leadership team might provide useful perspective in helping them to decide whether to refinance now or wait.

Examining interest rate swaps

In recent years, many religious institutions have secured fixed-rate financing by entering into an interest rate swap. As rates have declined, these borrowers have sought to refinance only to learn there is an “early termination cost” associated with refinancing their debt and terminating their interest rate swap prior to the scheduled maturity.

However, even if the “mark-to-market” is currently negative (in other words, you owe “early termination cost”), you might still be able to refinance to the benefit of your institution. A knowledgeable banker can explain how your swap might be restructured to a longer term, very possibly at a lower interest rate.

This is often referred to as a “blend-and-extend.” In such a scenario, the borrower’s loan balance does not increase, nor does the borrower need to write a check to pay the early termination cost. Instead, the termination cost is absorbed into the fixed interest rate from the new swap.

If your banker cannot explain this to your satisfaction, seek one who can.

Decisive action required

If you pass up the opportunity to refinance now, you might find yourself renewing your loan at a higher interest rate in the future. Seek a knowledgeable lender who can work with you to achieve a level of understanding that will enable you to make the best possible decision for your religious institution.

Dan Mikes is Executive Vice President and National Manager of the Religious Institution Division, Bank of the West, in San Ramon, CA.