By Dan Mikes

![]() As you might have noticed, interest rates have been on the move. Also, recent economic signals seem to imply the federal government will be more active in 2017. Consider comments economist Dr. Scott Anderson made on February 17 under the heading, “Inflation Runs Hot, Will the Fed?”:

As you might have noticed, interest rates have been on the move. Also, recent economic signals seem to imply the federal government will be more active in 2017. Consider comments economist Dr. Scott Anderson made on February 17 under the heading, “Inflation Runs Hot, Will the Fed?”:

The urgency to hike interest rates once again is ramping up in the United States on the heels of stronger than expected producer and consumer inflation in January.

January headline and core consumer inflation — at 2.5% and 2.3% from a year ago — hasn’t been this high in five years. Headline inflation’s climb has been even more impressive, climbing swiftly from –0.2% two years ago. Indeed, inflation pressure has visibly accelerated over the past year under a tightening labor market and stronger wage gains, a convincing rebound in energy and commodity prices, and accommodative monetary policy and financial conditions.1

No one knows exactly how much, how soon or how fast interest rates might increase. Against the backdrop of the rate movement, many leaders with religious institutions are likely wondering whether to break out of their interest rate swap and refinance now, before rates go much higher. Alternately, they could sit tight, avoid paying a swap “early termination

No one knows exactly how much, how soon or how fast interest rates might increase. Against the backdrop of the rate movement, many leaders with religious institutions are likely wondering whether to break out of their interest rate swap and refinance now, before rates go much higher. Alternately, they could sit tight, avoid paying a swap “early termination

fee,” and hope that interest rates are not much higher once their current swap matures.

I just used the term “early termination fee” — which might sound a bit foreign. Perhaps it is best to begin with some general information about what an interest rate swap is, and how it works.

A swap is a separate contract apart from the loan. The borrower pays the swap fixed rate and the swap pays the borrower a variable London Interbank Offered Rate, or LIBOR, plus the Loan Margin. This variable payment aligns with the borrower’s payment obligation on the underlying variable rate loan. Therefore, at its simplest, the swap might be considered a LIBOR hedge that essentially fixes the variable rate nature of the underlying LIBOR rate of the loan. The legal relationship is governed by the International Swaps and Derivatives Association, Inc. (ISDA) documentation.

The swap is designed to match your loan amount. So, if you make nothing more than regularly scheduled loan payments until the swap matures (the loan and swap maturity dates usually match), everything remains relatively simple. However, if you choose to make additional loan payments, or if you prepay your loan in full prior to the maturity of the swap, your outstanding swap amount will be larger than your outstanding loan amount, which means the swap amount will be larger than your outstanding loan balance. In this scenario, the bank might require you to reduce the swap. This reducing of the swap is referred to as “early termination.”

Generally, if rates rise after a borrower enters into a swap, the borrower might realize a gain (bank pays the borrower) upon early termination of the swap; or conversely, if rates stay the same or move lower, a loss might be incurred (borrower pays the bank), which might be substantial. Consequently, over the life of the swap, the swap has an inherent positive or negative value. This valuation is commonly referred to as the “mark-to-market (MTM).”

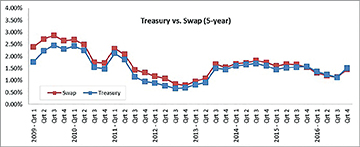

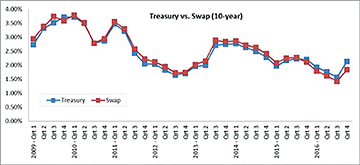

Take one quick glance at the historic interest rate graphs at left and you will realize that borrowers who entered into swaps between 2009 and 2012 probably

currently have a negative mark-to-market. Many of these borrower’s loans and swaps are now near maturity, and as they see rates rising, they are wondering if they should terminate their swap prior to maturity, pay the early termination cost, and refinance now before interest rates increase further. Borrowers often add these termination costs to the balance on their next loan. Alternatively, the borrower might write a check to pay the termination cost.

If your organization is considering refinancing now, but is facing an early termination cost, there is a refinancing option which you might not be aware of. You might be able to get a lower interest rate which is fixed for a longer term than what remains on your current swap, and you might be able to do this without adding that amount of the termination cost to your loan balance or writing a check for the termination cost. The termination cost is effectively absorbed into the interest rate on the new swap. This is commonly referred to as a “blend-and-extend.”

If your banker cannot explain the blend-and-extend to your satisfaction, seek one who can. Terminating your current swap and paying an early termination cost, might prove more expensive than doing a blend-and-extend swap. Now is the time to become informed on, and to consider, your options. Reviewing these options now might enable you to avoid paying a termination cost, and prevent the need to refinance at a higher rate down the road.

Reach out to an experienced lender who can assist you in expanding your knowledge, which can empower you to make the most appropriate choices for your religious institution.

1 Inflation Runs Hot, Will the Fed?, Scott Anderson, PhD, Bank of the West Economics,

Chief Economist

Dan Mikes is Executive Vice President and National Manager of the Religious Institution Division, Bank of the West, San Ramon, CA. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of Bank of the West.