By Rebecca M. DaVee, CPA

Our last metric is the sustainable operating metric.

Our last metric is the sustainable operating metric.

When you boil it down to the last key performance indicator — the one that tells the true story for sustainability — what is it? It’s not based on an account buried in the profitability of the organization, (i.e., statement of activities or profit and loss). Sustainability is revealed in the statement of financial position (i.e., balance sheet). The account that holds the accumulated reserves of the church is called a net asset (i.e., fund balance, equity, retained earnings). In any kind of business, the amount that remains after all the debt has been liquidated is considered the equity of the organization. What are the components of your church’s accumulated reserves that can be used for operations tomorrow, next week, next month, next year, and the years to come?

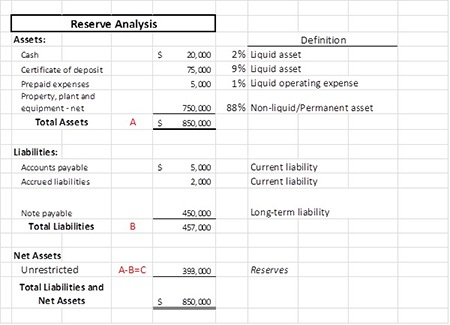

The following is an example of a typical balance sheet (i.e., statement of financial position) for a church. Let’s use simple math to calculate the reserves and then evaluate the detailed components.

Assets are what the church owns. Liabilities are what the church owes. As long as the church has more assets than liabilities, there are reserves. In the above example, the church has accumulated reserves of $393,000. since inception. The type of unencumbered assets always determine the quality of the reserves.

Assets are what the church owns. Liabilities are what the church owes. As long as the church has more assets than liabilities, there are reserves. In the above example, the church has accumulated reserves of $393,000. since inception. The type of unencumbered assets always determine the quality of the reserves.

Let’s determine the quality or components of the reserves. We must first evaluate the types of assets owned, and liabilities owed. In other words, are the assets current or long-term, and more importantly, how long does it take for those assets to convert to cash.

Cash is king. Cash represents the most liquid asset of an organization, and the resources to pay the

operating expenses of the church. Without cash, the church can’t pay employees or vendor invoices on time. Managing cash is critical to building reserves.

In the above example, we have defined the types of assets the church owns. Look at the key definitions above. Assets are defined as liquid (cash and cash equivalents), semi-liquid (converts to cash soon) or non-liquid / permanent (must sell or liquidate to convert to cash.

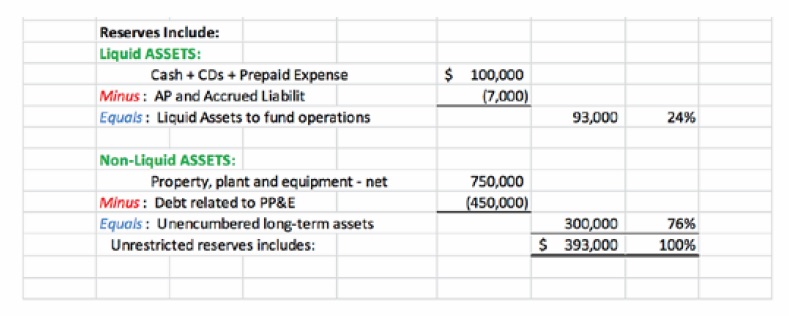

The following analysis tells us the church has $93,000 of available liquid reserves to pay ministry activities, and $300,000 has been invested in operating assets (property, plant and equipment). The critical issue is how many months of expenses can be paid from the liquid reserves?

Suppose the church receives an endowment restricted for maintenance of the sanctuary’s pews. An endowment is typically invested in income-producing assets (investments), and the income is used to comply with the donor’s restrictions. The endowment can never be part of the cash liquid reserves because they are permanently restricted.

Suppose the church receives an endowment restricted for maintenance of the sanctuary’s pews. An endowment is typically invested in income-producing assets (investments), and the income is used to comply with the donor’s restrictions. The endowment can never be part of the cash liquid reserves because they are permanently restricted.

Restricted / designated donor contributions always affect reserves. Be careful what type of donations you accept, and more importantly, understand the impact on your unrestricted reserves.

Some churches have a simple sustainable metric model, as reviewed above. Most churches have difficult, often complex, operating models. Understanding the components of your church’s reserves allows the executive team the ability to properly plan for current and future ministry activities, and more importantly, the funding risk.

That’s the sustainable metric — having unrestricted cash and related investments available to fund all future cash flow requirements. Whether you are looking at the past five months or the past five years, can you systematically determine your church’s funding needs? If not, you are only counting pennies on a short-term basis.

Rebecca DaVee is a partner with Salmon Sims Thomas & Associates. She has been working with churches, ministries, televangelists and other tax-exempt organizations for more than 30 years.