Many church leaders are facing a unique challenge in this new decade: how do you maintain giving when a global pandemic has church attendance at an all-time low?

Because we live in the digital age, however, church members have access to more giving options than ever before. Technology — like automated clearing house [ACH] payments — makes it possible to keep giving levels consistent, even in these uncertain times.

Sr. Director, Industry Verticals

Nacha

How can ACH benefit your church?

To find out, Church Executive recently partnered with Brad Smith, the Senior Director of Industry Verticals at Nacha, and Debbie Barr, the Senior Director of ACH Network Rules, Process and Communications at Nacha, to host a webinar: “Tithing in the 21st Century & the ‘New Normal.’”

In it, Smith and Barr explain the data revealing how ACH benefits churches, how tithing with ACH works and how to get started, and messaging tools to encourage your members to start giving via ACH.

Barr starts off the presentation with some background information on Nacha, the private sector rule-making organization that administers the ACH Network. Nacha came together nearly 50 years ago when several regional payments associations joined to create a national network covering the entire United States. In 2019, the ACH Network processed nearly 25 billion payments with a value of more than $55 trillion — which amounts to roughly 100 million transactions daily. ACH is a payment method popularly used by businesses, customers, and even the government, according to Barr.

So what can using this form of payment for gifts do for your church? Here’s some data to help answer that question:

-

Debbie Barr, AAP, CTP

Sr. Director, ACH Network Rules, Process and Communications

NachaResearch shows that 49% of all church giving is done by card online.

- ACH donors give more than double ($1,700 versus $650) in a 12-month period than those using paper check, credit card, or other means.

- 71% of ACH donors authorize automatic donations on a set schedule; compare this to only 9% of donors using other payment types.

- Members who donate electronically give more per person than those who give via the offering plate. During a recent Sunday service, the average check was $235. Of those who gave electronically, the average donation was $347.

- Donations made via ACH are more cost-effective for your organization than credit cards, as credit card donations can cost 3%-5% of the donation amount to process.

This last point is a big one. Essentially, instead of processing the payment from a credit or debit card, you’re going through the giver’s bank and withdrawing the gift as a direct payment from their account. How does that work? Smith breaks it all down for listeners in the webinar.

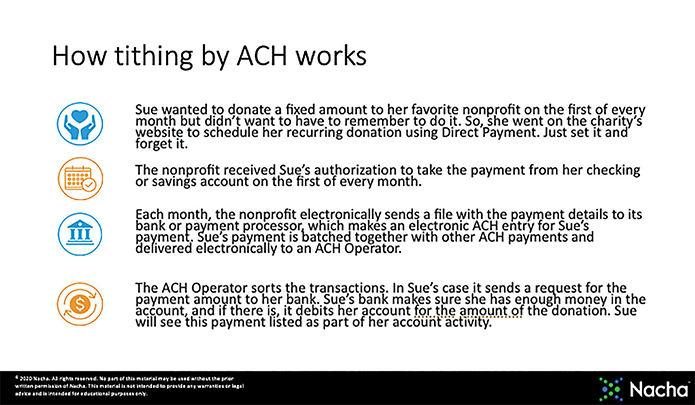

“We have trouble sometimes explaining the ‘how,’ so we created a slide as an easy way to try to tell you how ACH — and how tithing by ACH — works,” Smith said. (See below) “You can get this started by talking to your bank. If you already have a payment processor who does some of these online donations for you by card, you can talk to them and start doing some ACH.”

Barr and Smith encourage you to reach out to your bank or payment processors and set up ACH so that your church can become another success story like the two organizations discussed in the presentation: Mission Hills Church and Capital Public Radio. Both saw significant increases in donation amounts and frequency after implementing ACH as method of giving.

Once you’ve made this method available to members, the next step is to encourage them to sign up for ACH. Barr and Smith discuss how you can direct your messaging to make that happen. They also discuss a free toolkit you can access at ACHgiving.org, a website created by Nacha to help you understand and explain the benefits of ACH for giving.

To learn more, view the webinar on the Church Executive website at www.churchexecutive.com/webinars.

— Reporting by Skylar Griego

Questions?

Readers ask, experts answer.

How do I, as a church, approach my payment processor or bank to get ACH offered as a giving option?

Debbie Barr: Basically, every financial institution in the country has the ability to offer ACH, and many payment processors do also. But it’s not always the first choice they offer, so you’ll want to contact your relationship manager — whether it’s your financial institution or your payment processor — and ask if ACH is an option they offer. If so, ask how you can work with them to get set up for it.

How long does it usually take to get ACH started in a church?

Barr: It varies greatly depending on how much work your church does ahead of time to prepare. How much communication is happening, not only internally with your admin staff and your accounting staff, but also, how much communication you do with your members to get them thinking about it.

If you’re doing all that, the process can go very quickly once you reach out to your payment processor or financial institution.

How would you recommend promoting or offering ACH to church members, especially now that in-person worship is a limited or non-option?

Barr: One messages you’d want to share is that, even though we’re staying at home, there are still so many needs in our communities, and the mission must go on. Help them understand that ACH is a way to continue to fund the missions and to care for the community.

Another thing: with the pandemic going on, there’s a desire not to interact, unfortunately. By having an electronic payment such as ACH in place, giving is all done through the network, so it reduces that exposure. It becomes a safer, more sanitary giving option.

There are obvious financial benefits for introducing ACH to a church. Are there also benefits on the administrative end?

Brad Smith: There are. When people give cash or checks, it takes time to receive it, count it, and get it to the bank. I think the administrative benefit is a clear record of the payment, and it goes directly into the church’s account.

View the webinar!

Tithing for the 21st Century & the “New Normal”

Available now at www.churchexecutive.com/webinars

You say messaging ACH for new members is especially important. At what point in the assimilation process into the church do you recommend that?

Barr: I think it’s something you can mention early on, but not something to lead with. Instead, share with them all the missions you do, the community service — they’ll want to support the church’s work. Then, share all the ways that they can participate as a new member, including in-person, but also financial support.

If you only had a few minutes with a pastor, how would you explain why ACH is a good option for churches during these unprecedented times?

Smith: With ACH, we’ve found that donations more than doubled over a 12-month period. That’s because the majority of givers (about 70%) set a schedule for their gifts.

ACH is great for sustained donations. It’s cost-effective, and more money goes to the church.

Right now, people’s ability to give might change from month to month. Is it difficult for church members to make a change to their ACH giving schedule, if necessary?

Barr: No, not at all. The church would need to work with its payment provider to see what kind of timeframe would be required to make changes, but it should be fairly short. Just be sure that communication is happening between the member and the church, as far as, ‘I need to modify my donation this month / week.’

Let’s talk about data security. What makes ACH a good option for churches in this respect?

Smith: Givers’ information is stored and already encrypted, so the church never really has possession of information like routing number, financial institution or account number — it’s stored at the payment processor.

Even if your church works directly with that giver’s bank (if, say, it doesn’t have a payment processor), the information is still stored at the bank and subject to very strict data security policy through the Federal Financial Institutions Examination Council requiring the bank to ensure that data is encrypted.

In terms of data security, there are additional Nacha rules for organizations that do store that information. There’s a lot going on in the background that the consumer isn’t aware of, but we do it because security is of paramount importance to us.