On Dec. 20, 2017, Congress passed the Tax Cuts and Jobs Act (the “Act”) which represents the most substantial overhaul of the tax code since the 1990s. The Act brings significant changes to individual and corporate income tax filers.

How will the Act affect tax exempt organizations — and specifically, religious organizations?

Churches and ministries rely on public support (charitable contributions) to support their mission and related activities. Donors have been limited to 50% of their adjusted gross income on the amount of contributions to public charities and certain private foundations that could be deducted on their tax return. Prior to the Act, high-income-tax payers were often limited in deducting their charitable contributions and other itemized deductions. The “phase-out” limitation is now eliminated. Donors, who were “phased out” from charitable giving, might now be able to give more because of the added tax savings.

Under the new Act, charitable contributions of cash to public charities has been increased to 60% of adjusted gross income. So, one of the questions is, Will donors increase their charitable donations to take advantage of the amounts allowable by the new tax law? I believe the overarching question is this:

Will churches be the recipient of any tax savings from their members?

Since the 1st century, followers of Christ have been taught “to render unto Caesar what belongs to Caesar.” Old Testament scriptures emphasized the tithe, or 10% of a man’s earnings, should be brought to the Temple. Both teachings are promulgated by the modern church, including the saying, “It is more blessed to give than to receive.”

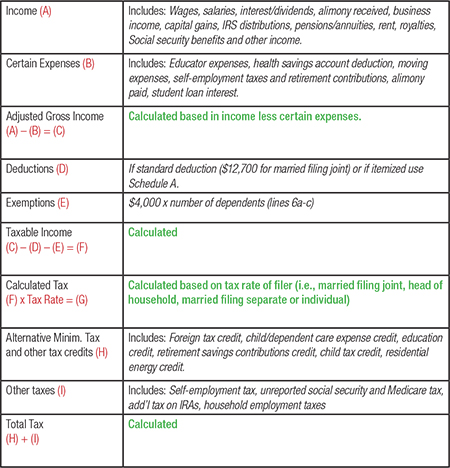

The American people have been promised that they will receive a tax cut, which translates to paying less federal income taxes. Income taxes are based on the following calculation:

What are the significant changes under the new Act that will reduce the taxes owed by filers? There are several significant changes that can affect the federal income tax.

What are the significant changes under the new Act that will reduce the taxes owed by filers? There are several significant changes that can affect the federal income tax.

Let’s look at the 2017 Form 1040 and identify the new regulatory changes starting with the repeal of exemptions. No longer will taxpayers receive a benefit for your dependents.

2017 tax filers can deduct exemptions from adjusted gross income in order to calculate the taxable income. For 2017, each dependent is worth $4,050 each. For 2018, exemptions will not be allowed — however, I believe that this allowance has been rolled up into the revised standard deduction discussed below.

2017 tax filers can deduct exemptions from adjusted gross income in order to calculate the taxable income. For 2017, each dependent is worth $4,050 each. For 2018, exemptions will not be allowed — however, I believe that this allowance has been rolled up into the revised standard deduction discussed below.

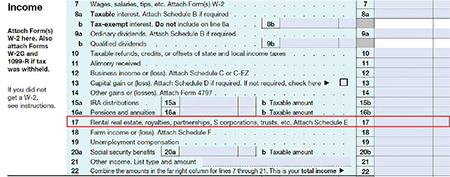

The current Income section of Form 1040 includes the following categories:

A significant change to items included in lines 7 – 22 relate to line 17. For tax years 2018 to 2025, individuals will be allowed to deduct 20% of qualified business income from partnerships, S corporations, or sole proprietorship, as well as 20% of qualified real estate invest dividends, qualified cooperative dividends, and qualified publicly traded partnership income.

A significant change to items included in lines 7 – 22 relate to line 17. For tax years 2018 to 2025, individuals will be allowed to deduct 20% of qualified business income from partnerships, S corporations, or sole proprietorship, as well as 20% of qualified real estate invest dividends, qualified cooperative dividends, and qualified publicly traded partnership income.

Items reported under the Adjusted Gross Income section of the return include:

Line 26 — moving expenses have been repealed and well as Line 31a — alimony paid. This means you cannot deduct these expenses from your income.

Line 26 — moving expenses have been repealed and well as Line 31a — alimony paid. This means you cannot deduct these expenses from your income.

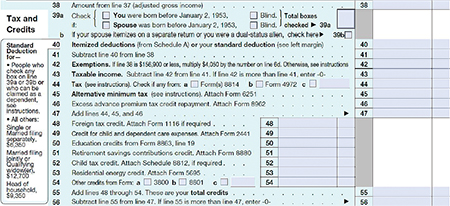

On page 2 of Form 1040 — Tax and Credits have historically included the following:

Under the Act the standard deduction (line 40) has been increased to $12,000 for single/married filing separately (compared to $6,350); $24,000 for married filing jointly or qualifying widow(er) (compared to $12,700); $18,000 for head of household (compared to $9,350). These revisions to the standard deductions might significantly reduce the number of filers who itemize their deductions.

Under the Act the standard deduction (line 40) has been increased to $12,000 for single/married filing separately (compared to $6,350); $24,000 for married filing jointly or qualifying widow(er) (compared to $12,700); $18,000 for head of household (compared to $9,350). These revisions to the standard deductions might significantly reduce the number of filers who itemize their deductions.

The alternative minimum tax (line 45) has been increased to $109,400 (married filing joint) and $70,300 for all other taxpayers.

Items deductions (line 40/Schedule A) include the following significant changes:

So, how will these changes to Schedule A affect donors? Will tax filers elect the standard deduction instead of completing/filing Schedule A? Deductions affect the calculated tax income (liability).

So, how will these changes to Schedule A affect donors? Will tax filers elect the standard deduction instead of completing/filing Schedule A? Deductions affect the calculated tax income (liability).

I suspect that donors who give substantial amounts to charities will continue to file Schedule A and be allowed to maximize their giving to 60% of their adjusted gross income. These substantial givers will benefit significantly under the new regulations.

Will these donors pass along their tax savings to the local church? Possibly. Why? Because these donors have supported their church and ministries and will now receive a higher tax benefit for their continued generosity.

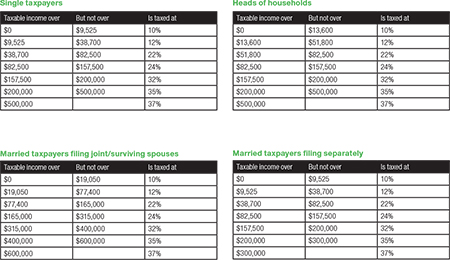

Tax rates for years 2018 thru 2025 have been lowered, which will also affect the taxes paid by Americans. These new rates are reflected as follows:

Another significant change included in the Act relates to estate taxes. The Act doubles the estate and gift tax exemption from $5 million to $10 million and will be indexed for inflation occurring after 2011.

Another significant change included in the Act relates to estate taxes. The Act doubles the estate and gift tax exemption from $5 million to $10 million and will be indexed for inflation occurring after 2011.

Corporate taxes have also been lowered under the Act, and these savings may be used to raise wages, hire more employees and invested in the facilities or products and services. The employees may reap some of these benefits and report higher income in their tax returns.

Why donors give….

Donors give to churches and other charities because they support its mission and because it is a spiritual value.

How well your local church will benefit from these changes depend on how well the leadership has taught their congregation to give generously / extravagently and how leadership stewards the church’s resources.

How well does your church communicate to the changing demographics of your congregation?

It’s just a choice…

Every donor has a choice where to deploy these tax savings.

The savings can be absorbed by the household budget, invested in savings / retirement accounts, or be used in the

local community.

If your church is meeting or exceeding its missional goals of seeking / saving the lost, extending mercy and love to others, and supporting the physical and spiritual needs of its community, then I suspect your church might benefit from the changes in the new Tax Cuts and Jobs Act of 2017.

Time will tell.

Rebecca M. DaVee, CPA, is a partner with Salmon Sims Thomas & Associates. She has been working with churches, ministries, televangelists and other tax-exempt organizations for more than 30 years.