By Rev. James R. Cook, CFP®

Do I buy a car or lease one? Do I work to pay for my education — or my children’s — or do I take out a loan? Do I rent an apartment or buy a house? For each of these questions, making the right decision depends on a number of factors that are unique to you.

But one financial question leaves us with very few choices: Do I save for retirement?

While most of us cannot say “no” to saving for the future, we can choose how much to save and how to make long-term savings a part of our lives.

“Never put off until tomorrow what you can do today.”

When it comes to saving, there are few hard and fast rules, but this old adage comes as close to a rule as you can get. Let’s illustrate with a story about two investors.

Joanna started her first job in ministry at age 25 after receiving a master’s degree. From her very first paycheck, she contributed $50 a month to her employer’s retirement plan. She did this faithfully for 20 years. When she turned 45, she stopped contributing and left the investment alone. At 65, she discovered that her account had grown to $76,472. Not bad since she had only contributed $12,000 and had not thought about it for 20 years.

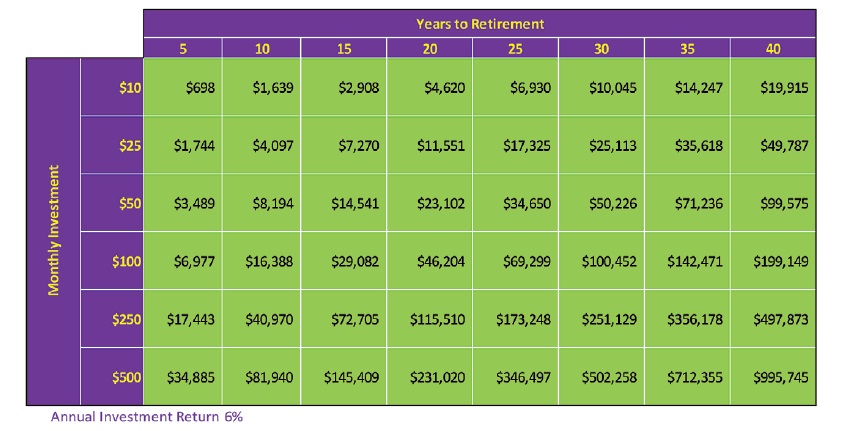

Joe was also 25; but when he began working, he had other priorities for his money and did not contribute to his employer’s retirement plan. At 45, Joe realized he needed to do something or he was going to have to work the rest of his life. For Joe to end up at age 65 with the same savings as Joanna, he needed to save $165 a month for the next 20 years. See the table (top) on the next page for the benefits of starting early.

Start with the end in mind

For most working people, Social Security will provide an amount somewhere between 30% and 40% of their final salary if they begin collecting at their full retirement age. For most individuals, the remaining funds required to meet living expenses will need to come from personal retirement savings.

You probably will only need to replace 80 percent of your final salary when you retire because you will no longer pay Social Security taxes — 15.3 percent, if you are a clergy person — and you will no longer be saving for retirement. Your personal circumstances and the lifestyle choices you make will ultimately determine your exact income needs in retirement.

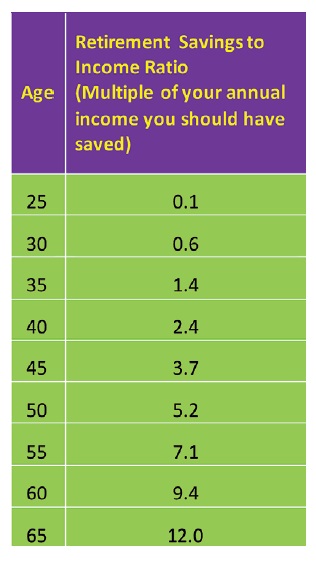

To support this level of income in retirement, you will need to save an amount equal to 12 to 15 times your final salary by the time you retire, assuming a retirement age of 65.

So, how are you doing? The table below gives an easy benchmark for various ages to illustrate where you should be if your goal is to reach 12 times salary at age 65.

Set a savings goal

Set a savings goal

Aim to achieve a 10-percent savings rate before the end of your 20s, a 12-percent rate during your 30s and 15-percent savings from age 40 to retirement. The good news is you can count any contributions your employer makes on your behalf toward this goal.

Of course, this model assumes an ideal — that you had the knowledge, foresight and ability to start saving with your first job sometime in your 20s. If you did not, and you were behind, you might need to save more to catch up.

Don’t let that scare you. With just a few modifications in your plan — like working two or three years longer or cutting expenses now or in retirement — you can make a big difference in achieving your goal. The most important thing is not to let disappointment about your current savings keep you from making changes. Remember: The sooner you start, the more you can save.

Make a plan and take your first step

You might want to save 12 percent, but are not anywhere near that. What can you do?

Here are four relatively painless steps:

#1: Forget about the past, and commit to working toward your goal starting today.

#2: Decide how much you can save each month out of your paycheck. Start by thinking about this in real dollars, not percentages.

#3: Next, add your savings amount and any amount your employer is contributing and convert this to a percentage of your salary.

#4: Make a commitment to reevaluate the amount you are saving annually with the goal of increasing it by 1 percent each year until you reach your target savings rate. If you get a pay increase, using part of that to increase your savings rate will be almost painless.

Saving for retirement is your choice. Take advantage of savings programs your employer offers. Start early by contributing an amount you can afford. Commit to increasing your savings whenever your compensation increases. Track your progress. Engage a financial planning professional to assist you. These simple steps can give you the retirement you choose.

Rev. James R. Cook, CFP®, is a National Outreach Manager at MMBB Financial Services. As a Certified Financial Planner™ professional, Cook is an expert in comprehensive financial and retirement planning. He is also an accomplished speaker and a passionate teacher with 10 years of pastoral experience in several California churches.