Navigating the newest challenges

By Gregory Love & Kimberlee Norris

On July 1, 2021, virtually every news outlet ran the story:

Boy Scouts Offer to Compensate Sexual Abuse Victims in Historic $850 Million Bankruptcy Settlement (USA Today)

Yet another reminder that sexual abuse risk demands our attention to implement effective prevention measures AND develop an insurance strategy.

Prior articles in our “Stop Sexual Abuse” Series in Church Executive have addressed a variety of issues and elements related to an effective safety system; this article will discuss the ever-changing environment involving sexual abuse risk and insurance.

Too often, ministry leaders lack an understanding of the insurance industry: terms, concepts, coverages, and roles of insurance players. In days past, that lack of understanding could be overlooked; no longer. In today’s climate related to child sexual abuse, the stakes are too high and the costs of making a mistake are too large. Church and ministry leaders must become good consumers and choose good partners to navigate this ever-changing landscape.

The reality of this risk has never been more evident. Avoiding common mistakes can prevent trauma to children and save resources meant to promote ministry fruitfulness.

UNDERSTAND INSURANCE ROLES

A good starting place is a description of insurance roles or players. In conversations with ministry leaders, we find ourselves explaining the differences between an insurance carrier, an insurance agent and an insurance broker. Being a good consumer starts with an understanding of the insurance partners with whom ministry leaders will interact.

Insurance Carrier

An insurance carrier is a company that finances or ‘carries’ the risk; an entity that issues the insurance policy. Some insurance carriers ‘write coverage’ for a broad variety of industries — from international shipping to sports injuries. Other insurance carriers are more specialized, choosing instead to focus on one or more particular marketplaces, like churches, social services or camps. Insurance carriers that specialize in the church and ministry sector develop products that are designed to meet the needs and risks unique to church and ministry programs.

Insurance Agent

An insurance agent works for an insurance company. On behalf of the insurance company, an insurance agent works with an applicant (i.e., church or ministry) to negotiate and purchase insurance products offered by the agent’s particular insurance carrier.

Insurance Broker

An insurance broker works for the insurance applicant (i.e., church or ministry). Like an insurance agent, an insurance broker will assist the applicant in negotiating and purchasing insurance products. Unlike the agent, the broker is not limited to a particular carrier; a broker can shop the church’s insurance needs among competing insurance carriers.

CHOOSE A ‘GOOD’ CARRIER

Best Practice: purchase coverage from an insurance carrier that regularly works with churches.

Approximately 10 insurance carriers provide coverage to churches, ministries and child-serving organizations as a specialization or business silo. It is our strong recommendation that churches purchase within this group. These carriers understand the particular insurance needs of churches and ministries and create insurance products (including coverages and policies) based upon these unique needs.

Case Study:

A mega church purchased insurance from a carrier that did not specialize in the church/ministry marketplace. The church’s primary concern was coverage for roof and storm damage related to a large campus. The best combination of roof and storm coverage for the property was provided by an insurance carrier that did not typically write coverage or create insurance products for churches. Consequently, the policy did not have the usual provisions for cyber-attack, child sexual abuse or embezzlement. This deficiency was not revealed until a multi-victim child sexual abuse claim was filed.

Within the group of insurance carriers focusing on providing coverage to churches and ministries, many provide policies with standard types of coverages that a ministry must have in place. The church must then negotiate limits and other unique coverage issues. Many insurance carriers NOT within this group are intentionally pulling out of the ministry marketplace, or at a minimum, choosing to NOT offer sexual misconduct coverage.

CHOOSE A ‘GOOD’ AGENT or BROKER

A good insurance agent or broker will be familiar with an applicant’s risk management and insurance needs. A good agent or broker should (1) understand child safety risks; (2) be able to make risk mitigation recommendations; (3) understand the church’s insurance needs — both coverages and limits; (4) navigate the application and renewal process; (5) understand the insurance carrier’s policy offerings vis-à-vis the church’s needs; and (6) understand how to shepherd the reporting of a child sexual abuse allegation to law enforcement authorities and the insurance carrier.

Ministry leaders must become better consumers. This starts with working with an agent or broker who understands sexual abuse risk, sexual abuse risk management and sexual abuse policy terms.

Best Practice: work with an insurance agent or broker who understands sexual abuse risk.

Case Study:

A nationwide outdoor ministry asked for a review of insurance coverage related to child sexual abuse risk. This ministry had been renewing coverage with the same insurance carrier for eight years relying on an insurance broker not familiar with sexual abuse risk or the unique terms of coverage.

We reported to the ministry executive team that the organization had Sexual Misconduct Coverage, but this coverage was narrowly defined to include sexual harassment only; the organization had no child sexual abuse coverage. Worse, they unknowingly had no coverage for the preceding eight years. Though the ministry changed brokers and obtained the correct coverages moving forward, this outdoor ministry has no child sexual abuse coverage for any allegation that may arise from the previous eight years.

LEARN THE TYPES OF COVERAGES

In 2010, insurance coverage for a child sexual abuse claim would be found within the overall limits in the general liability section of a policy. No longer. A variety of coverages associated with Sexual Misconduct now exist. Ministry leaders: be careful here; read the terms closely.

There are several types of ‘Sexual Misconduct’ that might be addressed by an insurance policy, including sexual harassment, sexual assault, inappropriate reporting of sexual abuse, improper supervision of a registered sex offender, inappropriate sexual relationships (i.e., affairs), peer sexual abuse, and inappropriate boundaries by counselors or clergy. Read the policy terms carefully to ensure that child sexual abuse is a covered risk (see above Case Study).

PREPARE FOR APPLICATION CHANGES

In the current insurance marketplace, insurance carriers know that abuse and molestation coverage is important to churches. Conversely, insurance carriers are aware that many churches and ministries are employing inadequate or ineffective efforts meant to prevent child sexual abuse. To access sexual abuse coverages and desired limits, churches must now demonstrate preparedness for sexual abuse risk, which occurs in the context of the application process.

To obtain or renew insurance coverage, a church or ministry must fill out an application. In the last year, many church leaders have noticed a growing number of questions related to sexual abuse risk: questions related to screening processes, background checks (depth of search and frequency of renewal), training for staff members and volunteers, and more. If you haven’t seen these questions … you will. Church leaders are learning that premiums are increasing and automatic renewal of sexual abuse coverage is not a given.

Why are insurance applications focused so heavily on sexual abuse prevention and why are premiums rising? The number of sexual abuse claims has skyrocketed, and the cost to resolve these claims has increased sharply … and there is no indication that either will subside. Case in point: the Boys Scouts of America plans to pay out $850 million; the bankruptcy filing kept the amount that low. For insurance carriers to continue providing coverage to child-serving organizations — including churches — child-serving organizations MUST take the necessary steps to protect children, thereby mitigating risk.

IMPLEMENT A CHILD SAFETY SYSTEM

Where child sexual abuse is concerned, a ministry’s primary motivation should be the protection of children. At the same time, simple availability of insurance coverage may provide a significant motivation for a church or ministry to implement an effective safety system addressing sexual abuse risk.

MinistrySafe advocates the use of a 5-Part Safety System, including:

1) Sexual Abuse Awareness Training;

2) Skillful Screening Processes;

3) Appropriate Criminal Background Checks;

4) Tailored Policies & Procedures; and

5) Systems for Monitoring and Oversight.

To learn more about the MinistrySafe 5-Part Safety System, visit www.MinistrySafe.com or download the Stop Sexual Abuse e-book at www.churchexecutive.com/ebooks#risk-management.

CLAIMS MADE vs. OCCURRENCE

When renewing coverage for child sexual abuse, ministry leaders must understand the difference between a ‘claims-made’ policy and an ‘occurrence’ policy. Understanding the difference between the two types of policies — claims-made and occurrence — can help avoid coverage gaps, particularly when changing from one form to another.

Claims-Made Policy

The claims-made policy covers incidents that occur after a policy’s start date and are reported to the carrier during the active policy period. A church may negotiate for a short ‘retroactive period’ that precedes the start date of the policy, and an ‘extended reporting period’ that would add an additional amount of time in which a claim can be reported to the carrier, and therefore be covered. Claims through this form of coverage must meet both criteria for coverage to occur.

Case Study:

Case Study:

A church purchased child sexual abuse coverage through a general liability policy on a claims-made basis year after year since 2010. The 2020 policy was effective from January 1, 2020 through December 31, 2020. A claim was reported during the policy period for a sexual abuse incident that occurred on February 5, 2020. In this example, the abuse claim was covered under the policy.

In many cases, however, sexual abuse allegations are not immediately reported. Often the incident of sexual abuse took place years or even decades before disclosure. If, in the aforementioned example, a sexual abuse incident occurred in 2017 but was reported in 2020, the sexual abuse incident will not be covered by the 2017 or the 2020 claims-made policy because the abuse occurrence and report did not occur within the same policy period.

A claims-made form of coverage is most valuable when the types of claims associated with a particular organization are immediately known and are generally brought to the organization’s attention in short order (i.e., vehicle accidents, slip-and-falls). Claims-made policies in the context of child sexual abuse are not advisable, given the time that often elapses between incident and report.

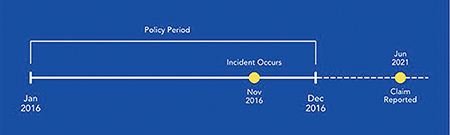

Occurrence Policy

An occurrence policy covers incidents that occur during the specific policy period, regardless of when the allegation is reported to the carrier. Keep in mind: under the terms of any policy, the church is required to report facts that could give rise to a claim; failure to do so can result in a denial of coverage.

Case Study:

Case Study:

A church purchased child sexual abuse coverage through a general liability policy on an occurrence basis year after year since 2010. A claim was reported in June 2021 related to an abuse incident occurring on November 20, 2016. In this example, the sexual abuse claim was covered under the 2016 policy, even though it was reported in 2021.

Best Practice: When renewing coverage — be sensitive to ‘term changes’ or ‘form changes’; subtle changes in words or phrases can be significant.

One recent circumstance involved a church whose carrier agreed to keep the premiums and the limits the same ($1 million /$3 million) — with one small change: the policy was modified from ‘occurrence’ to ‘claims made’. The policy period began on January 1, 2021. In 2021, the church will receive coverage for historical allegations through the past occurrence form coverages. In addition, the church will receive coverage for all allegations that occur and are reported to the carrier within the policy period (2021).

Any future insurance coverage will conceivably create a gap in coverage. For 2022, the church will either buy an occurrence form policy or another claims-made policy. Either way, any incident of child sexual abuse in 2021 that is reported in any year other than 2021 will receive no coverage. Of course, the church may be able to purchase an ‘extended reporting period’ (allowing the claim to be reported after the policy period), but these are sold at the sole discretion of the insurance carrier and usually involve months of extension, not years. In the future, this church will experience a gap in coverage for child sexual abuse incidents that occurred in 2021.

SEXUAL ABUSE FIRE DRILL

In classrooms across the country, school administrators lead faculty and students through mock disasters (fires, shootings, bomb threats, tornados, etc.) to ensure the existence of sound safety plans, communicate expectations to all involved and determine any necessary changes or improvements.

A failure to drill a foreseeable disaster can lead to catastrophic results, generally with little or no warning. In the midst of a crisis, it’s too late to prepare; the catastrophic event simply reveals whether the ministry took reasonable steps to prepare for the foreseeable event. One of the most common deficiencies revealed in a sexual abuse crisis relates to insurance: incorrect coverages, insufficient limits, failure to notify the carrier and claims-made vs. occurrence terms, among other issues. A fire drill related to sexual abuse insurance issues is essential for every ministry.

Insurance Fire Drill

Take the opportunity to ‘drill’ your church or ministry’s preparedness for a sexual abuse claim as it relates to insurance coverage. For this exercise, involve your insurance agent or broker. This drill might reveal whether you are currently in relationship with a ‘good’ carrier, agent or broker.

Assume your church receives a sexual abuse allegation. For purposes of this exercise, assume the allegation involves multiple victims and the accused is a trusted staff member or volunteer. As to existing insurance coverage, the drill is designed to answer these questions:

• Does your church have the correct coverages for a multi-victim claim?

• Does your church have sufficient coverage (types and limits) for a multi-victim claim?

• Are there endorsements, riders, limitations or qualifications related to sexual abuse coverage?

• Are the policies ‘claims-made’ or ‘occurrence’?

• Are there any gaps in coverage over the last 10 to 15 years?

Failures Revealed in Crisis

When a ministry fails to take the opportunity to ‘drill’ a foreseeable risk, deficiencies are typically revealed in the midst of a crisis. At this point, it is too late to make changes to insurance policies, coverages or limits.

Best Practice:

Evaluate your preparedness in advance of a crisis — especially as it relates to insurance coverage.

Case Study:

Several years ago, our law firm (Love & Norris) was retained by a large church addressing sexual abuse allegations related to a trusted staff member, with four female victims from 7 to 9 years of age. The fact patterns related to the abuse were conclusive and horrific, and we advised immediate care and support for the abuse survivors and their families. Church leaders made immediate efforts to address the trauma suffered by the victims.

When asked, church leaders indicated that the ministry had insurance providing $1million/$3million in coverage. When asked whether their insurance carrier was notified when the initial ‘facts’ came to light, leaders replied ‘no’.

At this point, it was too late to ‘drill’.

Several significant shortcomings were quickly revealed. The underlying policy did not provide $1million/$3million in coverage. Upon closer inspection, the policy included a specific ‘Sexual Misconduct’ provision which limited coverage to $100K/$300K for sexual abuse claims. The church had no E&O, D&O or Umbrella/Excess coverages.

Several significant shortcomings were quickly revealed. The underlying policy did not provide $1million/$3million in coverage. Upon closer inspection, the policy included a specific ‘Sexual Misconduct’ provision which limited coverage to $100K/$300K for sexual abuse claims. The church had no E&O, D&O or Umbrella/Excess coverages.

In the midst of this crisis, these leaders learned the church’s insurance coverage was grossly inadequate, and it was too late to supplement or improve coverage amounts. In this case, the insurance carrier tendered the $300K aggregate, satisfying its obligation under the policy. The church was forced to absorb defense costs and indemnity out-of-pocket, and quickly dwindled from a church with 36 full-time staff members to nine.

Before the crisis hit, ministry leaders should have had effective preventative protocols in place, secured sufficient coverage limits and considered purchasing additional supplemental and umbrella/excess policies. When asked about the church’s insurance broker, the executive pastor said the relationship was inherited from a predecessor. In the midst of the crisis, no one knew the identity of the broker or his contact information. It was later learned that this broker knew very little about sexual abuse risk, preventative efforts or related coverage solutions.

Value of the Fire Drill

The Fire Drill concept can be helpful in assessing insurance sufficiency and strategy. By thinking through a multi-victim allegation, a ministry can evaluate all insurance instruments for potential coverage (CGL, D&O, E&O, Excess, Umbrella, etc.), confirm limits, and clearly understand limitations, if any, providing an opportunity to secure appropriate coverages and limits. For some ministries, other creative solutions might be available.

REPORTING REQUIREMENTS

Ministry leaders should clearly understand state reporting requirements; ministry leaders should also know when to notify their insurance carrier as well as what information to provide. A timely and proper notification to law enforcement and a ministry’s insurance carrier is far more likely to occur when staff members are trained to understand the risk of sexual abuse and the common behaviors of sexual abusers. When leaders fail to report allegations of child sexual abuse to civil or criminal authorities, they further victimize abuse survivors and open themselves up to the possibility of criminal prosecution for failure to report. When leaders receive information related to an allegation and fail to notify their carrier, coverage and representation may be jeopardized.

SUMMARY

The stakes are high; children are at risk. Ministry leaders must understand this very important aspect of protecting the flock and preventing abuse of children in their care. Understanding, however, is not enough; ministry leaders must rely on good risk management partners — insurance carriers, agents and brokers — while navigating the ever-changing landscape of insurance products and strategies.

Kimberlee Norris and Gregory Love are partners in the Fort Worth, Texas law firm of Love & Norris [ www.LoveNorris.com ] and founders of MinistrySafe [ www.MinistrySafe.com ], providing child sexual abuse expertise to ministries worldwide. After representing victims of child sexual abuse for more than two decades, Love and Norris saw recurring, predictable patterns in predatory behavior. MinistrySafe grew out of their desire to place proactive tools into the hands of ministry professionals.

Love and Norris teach the only graduate-level course on Preventing Sexual Abuse in Ministry Contexts as Visiting Faculty at Dallas Theological Seminary.

Curious about the impact of gender self Id on this matter. For example, would the following scenario be a problem? https://www.google.com/amp/s/www.foxnews.com/media/california-parents-nonbinary-counselors-slept-camp-girls-education.amp

Having a sexual abuse fire drill sounds like a good idea. This could help keep people prepared. That training could come in handy when you least expect it.